Louisiana’s ‘Business-Friendly’ Climate Response: Canceled Home Insurance Plans

This story was originally published by Floodlight, a nonprofit investigative newsroom focused on climate accountability.

Louisiana homeowners will no longer have the assurance of holding onto their longtime property insurance policies after a damaging storm. And they could start seeing increases in premiums and deductibles since the state’s insurance commissioner convinced lawmakers to deregulate Louisiana’s insurance industry.

In the past, most Louisianans who purchased homeowners’ insurance could not be denied coverage, face larger deductibles or be burdened with repeated rate increases if their policies had been in effect for more than three years — a law that was unique to the state.

Starting next year, insurers are allowed to cancel up to 5% of their three-year rule policies each year in Louisiana, a state that has been hit repeatedly by devastating hurricanes.

These changes — approved by the Legislature and signed by GOP Gov. Jeff Landry — come at a time when households in many parts of the country are grappling with escalating property insurance premiums attributed to increased damage from climate-fueled storms and wildfires.

Explore the latest news about what’s at stake for the climate during this election season.

Consumer advocates say lawmakers have allowed the insurance industry to use the threats posed by climate change to make it harder for policyholders to get their claims paid when they need them most. The law changes also insulate the powerful insurance lobby, which could be an influential voice in demanding change to limit greenhouse gas emissions that fuel climate change.

Critics say the changes will propel Louisiana further into crises like California and Florida are already experiencing in their insurance markets. Most lending institutions require property owners to carry insurance, and some critics predict foreclosures and even more homelessness in Louisiana when most of the changes take effect in 2025.

The state’s Insurance Commissioner Tim Temple pushed back on those arguments, calling his solutions the “one narrow path” that will bring more choices to residents and rate stability to the state.

Since taking office this year, Temple has urged Louisiana lawmakers to create a more “business friendly” market. His ultimate goal: To cut the number of people who use the state program that serves as an insurer of last resort.

“I speak with consumers every day. Based on what I’m hearing from them and based on my own experience, insurance becoming too expensive for homeowners isn’t a potential future event — it’s the status quo and has been for quite some time,” Temple said.

While he acknowledges that increased storms and natural disasters are partially to blame for the higher rates locally and nationally, Temple said severe weather doesn’t fully explain why Louisiana’s market was doing so much worse than other states also dealing with increased weather threats.

“What does explain the gap is Louisiana’s reputation for excessive litigation and overregulation, both of which we’ve begun to address since I took office in January,” he said.

Insuring the Insurers Is Costly

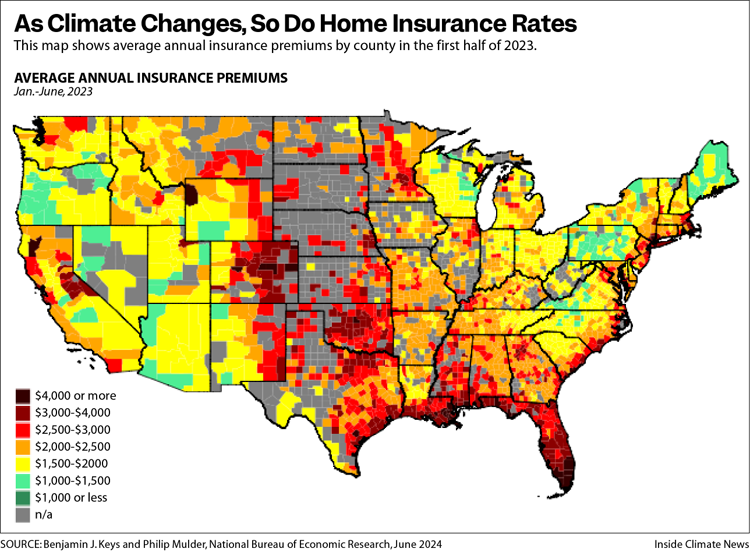

A recent study published by the National Bureau of Economic Research showed that, on average, annual insurance premiums have increased by 33% in the last three years — from $1,902 in 2020 to $2,530 in 2023. The sharpest increases were concentrated in ZIP codes with the highest disaster risk — many of them populated by larger nonwhite populations and lower-income individuals, the report states.

The report culled data from more than 47 million households’ mortgage escrow payments from 2014 to 2023. The authors say the top 5% of homeowners in areas with the highest risk of severe storms and wildfires could see their premiums increase as much as $700 by 2053 based on their conservative projections.

Study author Benjamin Keys, a professor of real estate and finance at the Wharton School at the University of Pennsylvania, agrees with Temple that the increased frequency and severity of weather-related damage isn’t solely to blame for the insurance crisis.

Keys, who in 2023 testified in front of the U.S. Senate Budget Committee, cited other factors including the rising cost of labor and construction materials to rebuild homes and the spiking costs of reinsurance — or the insurance that insurance companies themselves need to cover the cost of riskier policies. Many of those reinsurers are in other countries where they are not subject to U.S. regulations, said Keys, adding that reinsurance rates have been doubling each year since 2017.

“The insurance companies are scrambling. They’re scrambling to figure out: Now the price of offloading that risk has gone way up. Do we continue to work with these reinsurers? Or do we find ways to bear this risk than ourselves? Or alternatively, do we just leave those markets?” Keys said. “Now we’re seeing it kind of directly affect households’ bottom lines with insurers passing this cost on through insurance premiums.”

In his Senate testimony, Keys said rising climate-related risks coupled with escalating costs for reinsurance will continue. He said providers will continue to pass those costs onto policyholders — or exit local markets — leaving homeowners with fewer choices, less protection and more financial stress.

“Insurance companies are seizing on this moment in time where people are panicking about insurance, of being able to afford it and being able to keep it to, to push for things they’ve wanted for a long time: deregulation,” said Amy Bach, executive director of United Policyholders, a national nonprofit consumer advocacy organization.

Bach said state leaders should adopt more mandates, not relax them, to avoid an insurance crisis like what’s happening in California.

California Rates Shoot Up

Last year, Jamie Lafollette, a 35-year-old from Santa Cruz, California received the upsetting news that State Farm was not renewing the policy she and her husband had on their home for the previous 10 years. They had never made a claim.

Aware their community had been deemed a high risk for wildfires, Lafollette said she and her neighbors spent thousands of dollars fortifying their homes with concrete siding, fire-resistant roofs and creating buffer zones around their properties. But none of that seemed to matter when it came time for her to buy a new insurance policy.

Lafollette had been paying about $2,000 a year to insure their home. When she sought a new estimate, she was confronted with annual insurance rates of more than $20,000 a year.

Lafollete said since that eye-popping quote, the cheapest rate she’s seen so far was through the state-sponsored FAIR Plan at nearly $9,000 a year. Even that is too expensive, said Lafollette, who works for a nonprofit and whose husband is a disabled combat veteran.

“We’re panicking and we’re frustrated, because we’ve been working so hard to make our properties and our community fire safe,” Lafollette said. “The insurance companies don’t look at individual properties. They’re just looking at a category on a map. So it doesn’t matter if you’ve clear-cut your property or you’ve done all the work to make your property safe.”

California’s insurance commissioner has proposed that insurers be allowed to charge rates based on predicted future catastrophes — but only if they write more policies in high-risk areas. Companies also would be allowed to pass along the cost of reinsurance to customers.

In return, insurers would be required to factor in wildfire mitigation efforts at the regional, community and individual levels — like those undertaken by Lafollette and her neighbors — when setting rates, which must be approved by the California Department of Insurance. The rule package is expected to be finalized later this year.

Companies Flee Louisiana

In Louisiana, the home insurance market has struggled to rebound after at least a dozen insurers pulled out of the state following four major hurricanes in 2020 and 2021.

Janet Tobias, a 68-year-old New Orleans native, was among the thousands who lost coverage because her private insurer went belly up after Hurricane Ida in 2021. Fortunately, the retiree didn’t have to scramble to find coverage for her home.

The state’s insurance commission, under the tenure of former Commissioner Jim Donelon, had another insurer lined up for Tobias. But Tobias’ annual premium went from $4,000 to $11,000 a year, she said.

“This year they told us we can shop around, but when we shop around, they don’t have anybody to shop around to because they don’t have any more companies,” Tobias said. “So, it’s just a few companies, and all the prices are about the same.”

A survey published last year by Louisiana State University’s Reilly Center for Media & Public Affairs reported that 17% of Louisiana homeowners’ insurance customers surveyed said their policies were canceled; 63% had premium increases between 2022 and 2023.

And under the new changes in Louisiana, insurers can enact rate increases whenever they want, unless Temple, the insurance commissioner, rejects them within a 30-day review period.

John Ford, deputy commissioner for Louisiana’s Department of Insurance, said Temple can still deny rate increases for any reasons allowed under the previous system within that 30-day window. Ford said the goal is to make insurance available, affordable and accountable by setting clear expectations and working with insurers to make sure policyholders are treated fairly.

“He will not hesitate to take regulatory action when it is warranted,” Ford said.

State-Backed Insurance Targeted

Nearly 125,000 homeowners have been forced to take policies through Louisiana Citizens Property Insurance Corporation, the state’s insurer of last resort, since there are so few options in the private sector. It’s a huge increase since 2020, when the program had 34,373 policyholders.

But state-sponsored insurance doesn’t mean cheaper rates. Citizens is mandated to write policies that are at least 10% above the highest rates within each parish. State lawmakers suspended that 10% surcharge for the next three years for the vast majority of the state’s population, which is south of Interstate 10 on or near the Gulf Coast.

Temple said it won’t provide much relief given how unaffordable the state-backed policies already are. And Louisiana officials have been actively moving homeowners into private policies since 2008 to “depopulate” the state program.

“We need to get people out of Citizens, and the only way to do that is to have a competitive market,” Temple said. “The changes we made this session on the three-year rule and the claims process are major parts of a larger reform effort that is putting us on a path toward that competitive market.”

Local consumer advocates see a different future.

Ben Riggs, executive director of the nonprofit consumer advocacy organization Real Reform Louisiana, said the changes driven by Temple can’t logically accomplish the goals he lays out.

“If insurance company A drops a policy, Company B isn’t going to come behind them and pick up that policy; that policy is going to move on to Citizens,” he said. “You cannot solve an unavailability problem by forcing more people to insure with the last resort, it makes no sense. But that’s what’s going to happen by repealing the three-year rule.”

Riggs is predicting deregulation will mean widespread financial strain for a lot of low- and moderate-income households. He’s certain there will be homeowners forced to choose between feeding their children and insuring their homes.

Andreanecia Morris, executive director for HousingNOLA, said the changes could lead to more foreclosures or homeowners going without insurance because they can’t afford it.

“We’re looking at construction projects grinding to a halt. We’re looking at record homelessness and displacement,” she said. “We’re looking at homes not being able to be bought or sold because people can’t get insurance policies, while people are rushing to sell their houses.”

Tobias, the New Orleans retiree, hopes she can pay off her home to avoid the mandate that she have insurance, which she fears will soon become unaffordable. As she is no longer working, the hope of paying off the 15 years left on her mortgage is hanging on a prayer.

“I’m just believing in God,” Tobias said. “I believe in miracles.”

About This Story

Perhaps you noticed: This story, like all the news we publish, is free to read. That’s because Inside Climate News is a 501c3 nonprofit organization. We do not charge a subscription fee, lock our news behind a paywall, or clutter our website with ads. We make our news on climate and the environment freely available to you and anyone who wants it.

That’s not all. We also share our news for free with scores of other media organizations around the country. Many of them can’t afford to do environmental journalism of their own. We’ve built bureaus from coast to coast to report local stories, collaborate with local newsrooms and co-publish articles so that this vital work is shared as widely as possible.

Two of us launched ICN in 2007. Six years later we earned a Pulitzer Prize for National Reporting, and now we run the oldest and largest dedicated climate newsroom in the nation. We tell the story in all its complexity. We hold polluters accountable. We expose environmental injustice. We debunk misinformation. We scrutinize solutions and inspire action.

Donations from readers like you fund every aspect of what we do. If you don’t already, will you support our ongoing work, our reporting on the biggest crisis facing our planet, and help us reach even more readers in more places?

Please take a moment to make a tax-deductible donation. Every one of them makes a difference.

Thank you,

David Sassoon

Founder and Publisher

Vernon Loeb

Executive Editor

Share this article

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.

Title:Louisiana’s ‘Business-Friendly’ Climate Response: Canceled Home Insurance Plans

Url:https://www.investsfocus.com